Banco BPM will merge with Credit Agricole to create the second largest banking group in the country. After a series of rumors circulated by the messenger, the news has been confirmed by Corriere della Sera according to which the negotiations would be so advanced that it has also identified the governance of the new group in which Giuseppe Castagna would become CEO and Giampiero Maioli president.

J-Invest successfully completed a securitization of an NPL portfolio with a total gross value of €89 million. Founded in 2008, J-Invest’s objective is to achieve high returns mainly through the acquisition without recourse and the management of NPLs admitted to bankruptcy proceedings.

Illimity Bank S.p.A. announced in a press release the finalisation of the purchase of a portfolio of Non Performing receivables from Unicredit. The gross book value (GBV) of the transaction is approximately Euro 692 million and the type of receivables involved includes only corporate counterparties, guaranteed by real estate.

Intrum has released preliminary results for the third quarter should be substantially above the consensus of analysts, as published on the company’s website. The adjusted preliminary EBIT for the third quarter is SEK 1,687 million, which corresponds to an increase of 25% compared to the second quarter.

The deadline for suspending the activities of the Collection Agents expired on October 15, but the demands of taxpayers severely affected by the serious economic and liquidity crisis dictated by Covid 19 seem to have been heard by the Government that with the new decree issued on October 18 late in the evening gave back a breath of fresh air, extending again the period of ‘fiscal peace’. The resumption of the activity of the collection agents is now set, unless further extensions due to the resumption of the current pandemic, to January 1, 2021.

Are you interested in Italian banks and NPL/UTP market? Ask for a briefing (in person or via conference call) by sending me a private message. I am also available for consulting projects on Distressed Assets pricing and Portfolio Management.

Fintech Voice, the focus on fintech updates of Credit Village magazine will discuss the symbiotic relation between Fintech and Traditional banks: while in most traditional sectors, such as entertainment or retail, the advent of digital innovation has decreed the extinction of “dinosaurs” and the emergence of completely innovative new operators,, the financial services industry seems to be an exception to this paradigm.

Fire Group, approved the consolidated half-yearly financial report at 30 June 2020. Compared to first half of 2091 Ebitda is up by 16%, Asset Under Management up 15% Operating costs down by 11%. The main objectives for the year in terms of cost consist of an increase in margins and the finalization of the investments foreseen in the industrial plan, equal to 17 million euro.

Workinvoice, the Italian fintech that created the first marketplace for the exchange of trade receivables and YouDOX, the DocuMI electronic invoicing and storage platform chosen by over 275,000 economic operators in Italy, have jointly presented AnticipaMI an integrated solution for electronic invoicing, credit management and advance payment.

Users of the platform will be able to take advantage of an extremely streamlined and simple process of assigning trade receivables: once the invoice to be assigned has been selected, and the debtors and receivables have been analyzed to define the collectability and certainty of the receivable, it will be assigned to institutional investors and the company will obtain 90% of the nominal value of the receivable in 48 hours (the balance upon payment of the invoice by the client). In addition, the analysis of debtors and the predictive risk assessment developed by Workinvoice will allow companies to have more useful information to select the clients to work with.

The securitization operation consists of the granting by the special purpose vehicle company set up pursuant to Law 130/99 “HydraM SPV” of a loan with limited recourse in favour of AMCO and guaranteed by a portfolio of non-performing loans and probable defaults (the “Portfolio”) originating from Banca Monte dei Paschi di Siena S.p.A.. The Portfolio will be transferred to AMCO as a result of a partial corporate demerger.

Enel X Financial Services, an Enel Group company active in the design and promotion of innovative financial services, has signed a strategic partnership with SIA, a European hi-tech company leader in payment services and infrastructures controlled by CDP Equity, for the design and implementation of new mobile banking solutions.

Enel X Financial Services, is an electronic money institution (IMEL) authorized by the Bank of Italy in December 2018 that provides payment solutions to private and corporate customers, in full compliance with data protection and privacy regulations. It is also a regulated entity registered in the central register of the European Banking Authority (EBA) which contains information on payment and electronic money institutions

Prelios and General Finance have signed an agreement to support companies in temporary liquidity crisis classified as UTP. In particular, General Finance will be responsible for providing liquidity through the management and demobilization of working capital, helping to provide new financial resources to companies in difficulty, a fundamental element in their recovery process.

The commercial agreement is part of Prelios Group’s growth path in the UTP credit servicing market – a segment in which it is one of the first mover in Italy – aimed at maximizing the return to bonis of creditor companies and businesses. The ecosystem that will be created with the signing of the agreement between General Finance and the Prelios Group aims to support businesses and, more generally, the country’s economy to cope with the current particularly difficult macroeconomic scenario, helping to ensure liquidity for the production chains.

The merger between Sia and Nexi has been finally approved. The first is the company that builds and manages infrastructure and technological services for payment systems controlled by Cdp through Cdp Equity; the second is in fact the former CartaSì listed in the top 40 of Piazza Affari and is controlled by the Bain, Avent and Hourglass funds.

At the end of a negotiation that lasted about a year and a half, the shareholders of the two companies signed a memorandum of understanding that identifies the path that will lead to the merger. The new group resulting from the merger will have a capitalization of more than 15 billion, will manage about 120 million cards with 2 million merchants and over 21 billion payments processed.

The European Banking Authority (EBA) has published its quarterly dashboard covering data for the second quarter of 2020 and summarizing the main risks and vulnerabilities of the EU banking sector. While capital ratios have held up well, there are indications that the crisis has begun to impact asset quality. As the cost of risk increased, profitability continued its downward trend.

The fully loaded CET1 ratio increased by 30bps to 14.7% and recovered about half of the decline in the first quarter. The increase in capital ratios was supported by a contraction in risk-weighted assets (RWA) due, among other things, to regulatory measures such as changes in the support factor for SMEs.

In Italy, the volume of corporate investments in the first half of 2020 is around 3.5 billion euros with a variation of just under 35% compared to the first half of last year.This performance reflects the uncertain performance of the markets caused by the emergency health care due to the COVID-19 pandemic still in progress.

The payment gap is the time that passes between the agreed payment time and the actual transaction. The longer this period lengthens, the more companies suffer: 61% of Italian companies accept unfavorable payment terms in order not to lose customers against a European average of 69% and 43%, voluntarily, extend payment terms against a European average of 41%.

Are you interested in Italian banks and NPL/UTP market? Ask for a briefing (in person or via conference call) by sending me a private message. I am also available for consulting projects on Distressed Assets pricing and Portfolio Management.

Growing number of possible bankruptcies and credit defaults expected in the coming months is a critical issue, which could undermine the recovery path of the European economy in the delicate phase following the lockdown measures,

ECB’s more conservative estimates predict growth of up to 1400 billion for the stock of new impaired loans, while a survey carried out by the consultancy firm PWC quantifies the volumes expected for Italy in the next 12-18 months at up to 100 billion.

The phenomenon is worrying for two main reasons: on the one hand, the reduction in Gross Domestic Product due lower value added by bankrupted firms and the decrease in tax revenues due to the decline in income and profits, on the other hand, financial institutions are likely to reduce the amount of funds they can make available to the economic system in the very moment in which when there is a high need for liquidity, because they are forced by strict regulations to allocate significant amounts of capital to cover expected credit losses.

In particular, credit institutions find themselves in an uncomfortable position, which is also a dilemma for supervisory authorities and national governments:

– focusing on stability and risk management , implies a potential reduction in the supply of credit to the entire economic system and in particular to those firms who may need it most

– using less restrictive criteria in lending to corporations struggling to survive and, broadly, to support the economic recovery, entails the risk of excessive deterioration in credit quality which may disrupt banks’ balance sheets

How to get out of this deadlock?

During a round table held last September 25th, Valdis Dombrovskis, Executive Vice-President of the European Commission stressed the need to intervene in a timely manner:

If we fail to act in time, we could see the consequences of the last financial crisis repeating themselves and NPLs would rise on banks’ balance sheets would rise for years afterwards.

That would undermine our financial stability and the entire economic recovery.

Speech by Executive Vice-President Valdis Dombrovskis at the roundtable on tackling non-performing loans

So far, solutions demanded by lobbyists and bankers, and discussed within the institutions range from the “Bad Bank” hypothesis, in the centralized version at European level or declined through a series of national operators (in Italy there is already AMCO company owned by the Ministry of Treasury born in 1997 as SGA to clean up the Banco di Napoli) to changes in current regulations considered too strict: few weeks ago Alberto Nagel, CEO of Mediobanca, said that calendar provisioning is like “an atomic bomb in the balance sheet of banks” .

In the first case, the idea is that banks offload bad debts onto some public institution that will also bear (probably at taxpayers’ expense) the additional losses associated with this burden.

In the second case, it is a matter of allowing larger flexibility on default definition (when a credit is qualified as non performing) and expected loss forecast ( how much banks are going to recover on non performing loans): this would mean to undo the remarkable progresses made by by regulators and supervisory authorities in recent years.

So far, there has been a negative feedback from authorities on the hypothesis of softening the rules because of a clear risk of undermining the solidity of financial intermediaries by triggering a dangerous “domino effect” that starts from the corporate debtors, is transmitted to the banks and could risk involving national governments, and this would frustrate the past efforts to make the system more transparent and stable after the last sovereign debt crisis in Europe.

There seems to be greater openness towards solutions that, at least on a theoretical level, can replicate market mechanisms by requiring that the loans divested by banks are assessed as independently as possible so as not to transfer undue losses to taxpayers.

In particular, in the Dombrovskis speech we read two suggestions to address the problem:

Overall, I believe that the strategy should focus on two areas:

Firstly, to develop secondary markets for distressed assets.

Here, I would urge the European Parliament to reach agreement on the proposal for a directive on credit services and credit purchasers. This should be a top priority.

Secondly, to further reform the insolvency and debt recovery frameworks. Here, we should build on the results of the ongoing benchmarking exercise to discuss targeted national measures.

These will play a key part in tackling NPLs over the longer term, combined with a rapid agreement on the proposal for a directive on accelerated extra-judicial collateral enforcement.

Speech by Executive Vice-President Valdis Dombrovskis at the roundtable on tackling non-performing loans

The dilemma therefore concerns a profile that we have already discussed on this blog:

banks play a key role within the economic system (credit supply and transmission of monetary policy) and this is the reason why they are subject to specific rules especially regarding resolution and insolvency frameworks in order to defend whole system stability.

Defending banks involves transferring a series of burdens to other parties, from consumers to taxpayers, and when this is not strictly justified by concrete risks to the stability of the system, it could grant an unfair advantage for banks and their shareholders.

The way to deal with this difficult situation, maintaining as far as possible a balance of different interests and avoiding abuse and distortions, necessarily passes through a careful mix of transparency, accountability of financial intermediaries and modulation of public intervention

In terms of transparency, the regulatory effort in recent years has been directed towards ensuring that, especially with reference to banks in Mediterranean countries, there were no longer doubts and uncertainties regarding the quality of their loans (how much is truly Performing, how much is simply Unlikely to Pay, and above all how much is really Non Performing ) and the adequacy of the capital.

This should avoid new cases like Monte dei Paschi di Siena and the Popolari Venete.

It is not the case to go back on this point, not even for the Pandemic, because a fair representation of credit quality is a mandatory requisite in order to to determine the extent of the losses actually expected and the capital required to compensate them.

As far as accountability is concerned, it cannot be an accounting rule or an extraordinary intervention by the state to assess whether or not a company is able to recover and meet its obligations. It is up to the banks to decide to whom they grant and withdraw credit and to bear the consequences of this choice. In difficult circumstances such as those we will be going through in the coming months, it is essential that this role is not lost and that it does not degenerate into the extreme excess of avoiding any risk by interrupting the granting of credit, nor the opposite extreme of artificially keeping insolvent counterparties alive.

State intervention should be concentrated on offsetting the negative effects of the exogenous shock, without fuelling unfounded expectations, but rather actively supporting the transformation and reconversion of business activities that are no longer appropriate to the new context.

Before the spread of the pandemic, financial intermediaries were going through a delicate transition phase, in order to survive in a world characterized by low interest rates, strong competition from innovative operators and the need to deploy new energy, resources and technologies to correctly measure risk.

Health emergency has accelerated this process and enlarged problems for less innovative financial institutions: the best way to overcome this critical moment need to pass through the search for solutions adapted to the new environment and any attempt to hide behind emergency legislation or state subsidies will enlarge the cost of adjustment and postpone the time of resolution.

Are you interested in Italian banks and NPL/UTP market? Ask for a briefing (in person or via conference call) by sending me a private message. I am also available for consulting projects on Distressed Assets pricing and Portfolio Management.

La finanza in soldoni è un Podcast e una Newsletter di educazione e informazione finanziaria a cura di Massimo FamularoNell’episodio di oggi della rubrica prendo spunto dalla chiusura in negativo delle borse di venerdì scorso (a cui è seguito un parziale rimbalzo all’inzio di questa settimana) per fare qualche riflessione: è arrivata la correzione che tanti annunciavano? Quanto durerà? Se questo il progetto vi piace potete segnalarlo nei commenti ai video Youtube e iscrivendovi al canale di Massimo Famularo.Entra a far parte del supporters club al costo di 3 euro al mese sostieni il podcast che rimane liberamente accessibile a tutti e accedi ai contenuti premium che includono la condivisione delle mie scelte personali di investimento,https://www.spreaker.com/podcast/la-finanza-in-soldoni–4367617/supportNel secondo episodio del podcast riservato agli iscritti al supporters club parlo del titolo Mercadolibre e condivido la mia posizione in merito alla convenienza di detenerlo o di acquistarloVi ricordo che troverete anche commenti su azioni singole che scelgo a titolo personale dietro il paywall della Newsletter Canale TelegramSostieni il progetto con una donazioni anche a mezzo bonifico bancario, richiedi IBAN scrivendo a mfamularoblog@gmail.comLa Finanza in Soldoni è un progetto multicanale che include Podcast Newsletter playlist sul canale Youtube di Massimo Famularo un libro disponibile nelle principali Librerie e Bookstore on lineSuggerisco anche la lettura delle "Storie di Tutti i colori più uno"Il mio Blog è MassimoFamularo.com

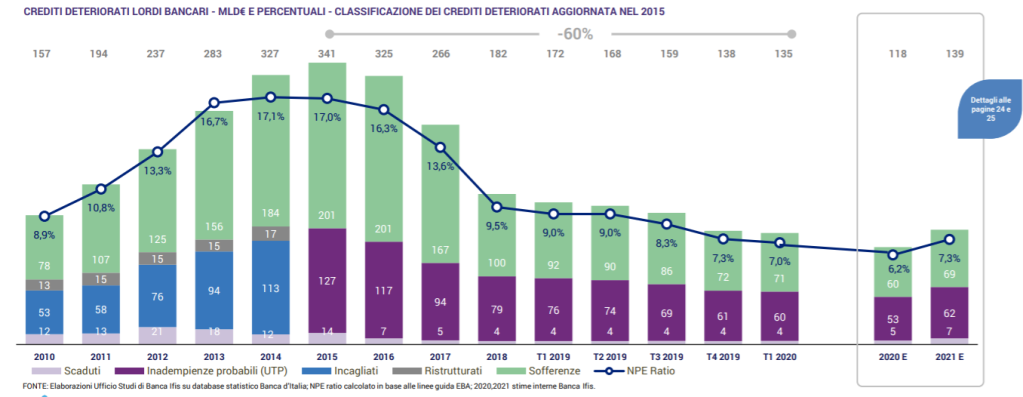

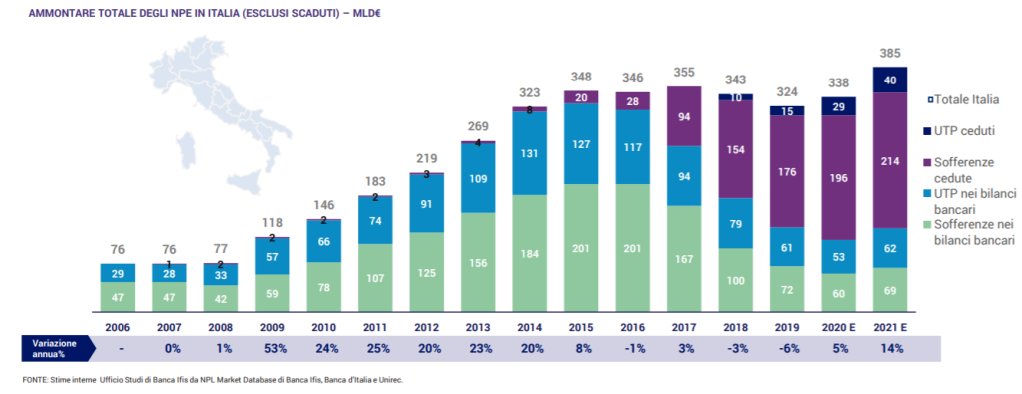

1- The decreasing trend in NPE ratio started in 2015 will be reverted in 2021 when it will rise back to 7.3% from the minimum level of 6.2% expected at the end of 2020

2-Public intervention has delayed the impact of COvid19 and Lockdown measures that will become manifest in 2021

3-The total stock of NPE (including both banks and investors) will reach an all time peak in 2021 at 385bn

The expected new wave of Non Performing Exposures will be a remarkable challenge for banks also because most recent updates in regulation (especially regarding calendar provisioning and default definition) will not be amended to consider current extraordinary situation.

European Commission and ECB will try to promote incentives to develop secondary market and this may include web based marketplace as well as state sponsored asset management companies (I discussed the topic in this post) .

Credit management industry is also about to face a challenge because the substantial increase in the total NPE of the system will happen while the whole economy will be trying to recover from the strong recession caused by covid19 and Lockdown measures.

This could be a good opportunity for those servicers able to handle increased volumes maintaining acceptable levels of performance and for those specialized in segments where competition will not erode profit margins.

The need for large investments (especially in technology) and common cost structure of incumbent large special servicers will most likely favorite a further consolidation in the market.

Are you interested in Italian banks and NPL/UTP market? Ask for a briefing (in person or via conference call) by sending me a private message. I am also available for consulting projects on Distressed Assets pricing and Portfolio Management.

If you like my updates you can buy me a coffee clicking on the button with the small mug below

Reuters reported thatEuropean Central Bank (ECB) is working on an Amazon-style website to sell hundreds of billions of euros of bank loans.

The project should be aimed at increasing the competition on Bad loans secondary market an is expected to be discussed with European Union officials on Friday 25th.

The large number of new NPEs expected in next month due to the impact on economy of Covid19 Pandemic and Lockdown measures may pose a substantial challenge to European Banks that need also to comply to ever tighter regulation on capital and provision.

National government are quite worried for this topic and France and Germany have called on the European Union to ease bank capital and bonus rules to avoid crimping the flow of credit to an economy trying to recover from the coronavirus crisis, a paper seen by Reuters showed.

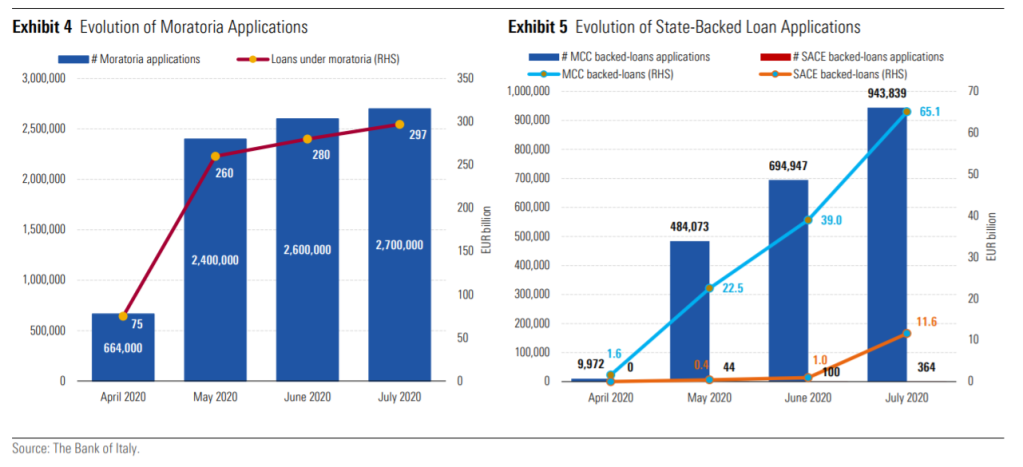

Italian Banks, as stated by Morningstar DBRS, reported a an aggregate net loss of EUR 464 million compared to a net profit of EUR 6.2 billion in the same period of 2019 and supported the Economy handling Moratoria files and State Baked loand

The improvement of Bad Loans secondary market has been a high priority for European Banking Authority (EBA) whose former chief is now head of ECB Banking Supervision and has been supporting the idea of a “Bad Bank” solution based on Asset Management Companies.

Some kind of Extraordinary Measure is widely expected but at the moment market oriented solutions like “the Amazon of Bad Loans” seem more likely than those involving heavy organizations.

I discussed in a previous post the rumors regarding the European Bad Bank pointing out that some non negligible details should be taken in consideration (recovery cost, quality of credit management etc) and that solutions like GACS (italian state guarrantee scheme) are less distortive of market prices.

An “amazon-like” marketplace may seem a good idea and for sure is based on the correct target of increasing competition, nevertheless some specific issue shold be considered

1- Bad Loans are illiquid assets that need detailed due diligence to be properly assessed and specific expertise to be managed this mean that only a limited amount of competitors looking for high yields can access the direct purchase and would be interested in this platform

2-So far Securitization has proved to be the best mechanism to build a liquid market from illiquid assets and a proper tranching of notes would open the door to a number of potential investors way bigger than those potentially interested in accessing the new marketplace

3-The idea of a single wider market is attractive but so far law, procedures and economic environments of European countries are still quite different and require local knowledge to event start thinking of investing in NPLS

European Banks will probably need some help and some kind of extraordinary measure to handle the Bad Loans problem will probably be introduced in order to

Are you interested in Italian banks and NPL/UTP market? Ask for a briefing (in person or via conference call) by sending me a private message. I am also available for consulting projects on Distressed Assets pricing and Portfolio Management.

If you like my updates you can buy me a coffee clicking on the button with the small mug below

Are you interested in Italian banks and NPL/UTP market? Ask for a briefing (in person or via conference call) by sending me a private message. I am also available for consulting projects on Distressed Assets pricing and Portfolio Management.

If you like my updates you can buy me a coffee clicking on the button with the small mug below

Bad Bank is magic word for politicians and a wet dream for bankers and banks’ shareholders: it basically mean that taxpayers money will be used to foot banks’ losses.

There will always be proposals and research papers stating that this is not the case, well anytime you find them just ask few questions:

1- how will the transfer price be calculated and how can we check if the price is rigged?

2-who is going to pay recovery cost (legal, administrative, etc) and how can we check if them are inflated ?

3- provided that healthy markets for distressed assets do exist in Europe why do we need a public entity to interfere with them?

If you are not sure that taxpayers’money are going to be involved pls check Occam Razor: if a Bad Bank truly trades at market prices, why market players with better expertise, remarkable track record and risk appetite should not compete? If the price paid by bad bank is fair and causes relevant losses to the seller what is the benefit for the banks?

The common answer is that a public bad bank does not need to seek profits so can pay higher prices but the main fallacy is that this assumes a market liquidity that by definition is non existent when you deal with illiquid assets. It also does not take in consideration that the lack of technical skills in managing credit recovery can offset the margin granted by not working for profit.

Market price of illiquid assets is not only driven by current market conditions (interest rates, availability of funds etc) but also by the ability of asset manager to extract value from them: that is the weakest point in bad banks solution.

If the bad bank do not involve market players to extract value it is likely that it will get poor results.

If it do involve market players, what do we need its intermediation for?

These arguments can explain why in 2016 European Commission rejected the idea of a bad bank for Italy and agreed a different instrument aimed at mimic as much as possible market dynamics the GACS (Garanzia sugli Attivi Cartolarizzati) that so far have proved more efficient than any bad bank solution.

But the main reason why a Bad Bank should be considered an obsolete tool to handle EU Bad Loans is that a mechanism that proved far better is available and could be easyly applied out of italy.

My best guess is that on 25th september the most reasonable solution should be a guarantee scheme similar to GACS that could be applied at a EU wide level.

Most relevant benefits would be:

1. Banks allowed to derecognize bad assets as if they had sold by simply transferring (often at close to NBV values) them to securitization vehicles sparing immediate losses (and consequent need for public money or capital increase) caused by actual sale

2. Public intervention limited to a guarantee (that may even not be enforced if everything goes well) aimed at providing immediate relief to banks with very limited distortion of market processes

3. Wide involvement of market players (special servicers, rating agencies, debt purchasers etc) to ensure transparency and transfer values close to market equivalent

Recent Italian experience also shows that a secondary market for Non Performing Exposure in Europe do exist and can handle large volumes.

Therefore the most relevant reason why a a GACs like solution is better than a bad bank is that it would not replace market forces but use them to price illiquid assets as close as possible to open market equivalent values.

Are you interested in Italian banks and NPL/UTP market? Ask for a briefing (in person or via conference call) by sending me a private message. I am also available for consulting projects on Distressed Assets pricing and Portfolio Management.

If you like my updates you can buy me a coffee clicking on the button with the small mug below

Are you interested in Italian banks and NPL/UTP market? Ask for a briefing (in person or via conference call) by sending me a private message. I am also available for consulting projects on Distressed Assets pricing and Portfolio Management.

If you like my updates you can buy me a coffee clicking on the button with the small mug below

Are you interested in Italian banks and NPL/UTP market? Ask for a briefing (in person or via conference call) by sending me a private message. I am also available for consulting projects on Distressed Assets pricing and Portfolio Management.

If you like my updates you can buy me a coffee clicking on the button with the small mug below

Proud to be attending as moderator at the Finance TV Week in the session on UTP exposures on 9th July at 3:30 pm.

The event will see an outlook of Italian NPE Market by PWC that will

The Round Table on UTP will be moderated by myself and Manuela Donghi financial Journalist of Le Fonti TV and will involve 4 speakers:

Francesco Lombardo-Partner Freshfields Bruckhaus Deringer LL Riccardo Marciò- Responsabile Direzione NPL – Banco Desio SpA Antonella Pagano – Managing Director at Accenture Italia Andrea Tresoldi -Head of UTP Business

The event will be in web streaming on this page and on TV channel Le Fonti TV. Questioons to speakers can be submitted at this email inviti@lefonti.it

Are you interested in Italian banks and NPL/UTP market? Ask for a briefing (in person or via conference call) by sending me a private message. I am also available for consulting projects on Distressed Assets pricing and Portfolio Management.

If you like my updates you can buy me a coffee clicking on the button with the small mug below and subscribe my newsletter